The South Korean Nuclear Industry

South Korea runs one of the world’s most efficient and cost-effective nuclear programmes. But with limited plans for expansion, is this a model of restraint or a missed opportunity?

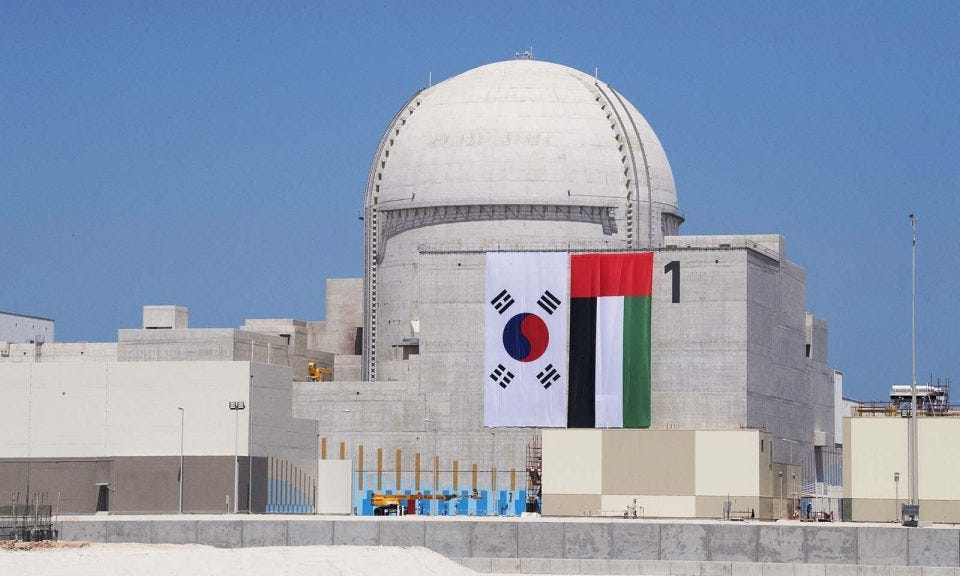

Barakah-1, the first Arab commerical nuclear reactor, powered by a Korean APR1400 designed by KEPCO.

South Korea is one of the most important industrial economies. It is the world's second-largest semiconductor producer, championed by Samsung Electronics and SK Hynix, manufacturing chips foundational to modern civilization. Behind China and the China State Shipbuilding Corporation, its shipbuilding industry, led by Hyundai Heavy Industries, Hanwha Ocean, and Samsung Heavy Industries, is the second largest by number of new vessels. South Korea retains a competitive steel industry through POSCO, the world's eighth-largest steel producer. Underwriting this advanced and varied industrial economy is cheap and reliable electricity provided by the Korean Electric Power Corporation (KEPCO), which has developed a world-class nuclear industry, principally managed by its subsidiary Korea Hydro & Nuclear Power (KHNP). Unlike other countries, which directly subsidise nuclear-generated electricity, standardised designs, clear political support for future nuclear generation, consistent political backing, and steady construction cadence have created a system where nuclear power remains not only low cost but financially sustainable. Although sold at prices set by the state, nuclear electricity is not only cheap but profitable for KEPCO overall.

The current flagship reactor, the APR 1400, is the Western world's most cost-effective reactor, costing between $2.2 and $2.8 million per MW when built in Korea. Although the upfront cost is significant per reactor, nuclear generation averages over 90%, and the Shin Hanul Unit One ran at 99.3% in 2023. Levelised cost of electricity estimates for Korean nuclear are USD $42-50 per MWh, far cheaper than gas, coal, or hydroelectricity generation. KEPCO has successfully exported the APR 1400 to the UAE and is exploring further exports with Poland and the Czech Republic. Korean reactor components are manufactured primarily by Korean firms. In combination with its highly capable defense sector, South Korea’s civilian nuclear program could supply the material and engineering base needed for a rapid nuclear weapons breakout if strategic conditions changed. Korea's deficiencies in natural resources such as natural gas and coal, which are key motivators for a varied electricity supply, also extend to domestic uranium mining production, but it maintains a fuel stockpile for up to five years.

While Korea is not planning to greatly expand its nuclear fleet, aiming for only 35% of total electricity generated by nuclear power by 2036, its nuclear industry would be well-positioned to deliver a far larger civilian nuclear buildout. In contrast to China, Korea could generate nearly all its required power demands through nuclear generation, easing its planned transition to a low-carbon-emitting economy by 2050 without affecting global uranium supply or risking its economy, which in 2023 was 24.3% based on manufacturing, on a volatile, complex, and variable renewable-based grid. South Korea’s nuclear industry should be the envy of the Western world, but its success is legible and replicable with sufficient political will.

South Korea’s nuclear power journey.

South Korea was not always a developed, high-tech industrial economy capable of efficiently producing industries that Western countries struggle to retain. Its limited natural resources, protectorate status under Qing China, and remote location meant it was not a target for Western Imperial ambitions. But this same isolation left it unable to resist the rise of Japanese power, which had embraced Western industrial and military ideas following the Meiji Restoration. After Japan defeated both China in the First Sino-Japanese War (1894–95) and the Russian Empire in the Russo-Japanese War (1904–05), Korea was established as a protectorate before being annexed in 1910. Japanese rule did not result in development of the Korean economy, and coupled with increasingly extractive Japanese policies during the Second World War, in the post war period it was desperately poor but split between the Communist sphere of influence in the North, which became the Democratic Peoples Republic of Korea and American backed regime in the South. The bitter colonial experience of Korea, marked by repression, forced labour, sexual slavery, and cultural erasure while being ruled by Japan, still resonates to this day.

Myeongdong in central Seoul in 1950. The district is now an international shopping hub (Limb Eung-Sik/NYT.)

The South's weakness led the expansionist regime in the north under Kim Il Sung to launch an invasion in 1950, which was repelled and fought to a bloody stalemate in 1953, with an armistice but no peace treaty. After the war, South Korea remained weak, dependent on foreign aid, with little industry, and ruled by authoritarian Syngman Rhee. Due to its weakness and to defend it from North Korean aggression, in 1958 the US placed MGR-1A surface-launched missiles, capable of delivering a 20kt nuclear warhead. After the instability of his regime led to a short-lived second democratic government, a military coup by the second-in-command of the South Korean Army, Park Chung Hee, in 1961, left South Korean prospects looking bleak. Park Chung Hee, like many leaders in the 1960s, had ambitious dreams of economic development and industrialization. However, South Korea lacked natural resources, was dependent on the US for aid, and faced a then-formidable hostile country on its northern border. Remarkably, unlike other leaders of the time, he was able to create a miracle. With tight control over the business elites of South Korea, he pushed their family-controlled businesses (Chaebols) to pursue textiles, apparel, electronics assembly, and light engineering manufacturing while normalising relations with Japan, which unlocked a critical flow of grants, loans, and reparations that helped finance industrial growth. As this strategy succeeded, and South Korea's economy grew at an annual rate of 9.7%, Park moved to develop heavier industry, but also required growing electricity to power this industrial explosion.

After Park had taken power in 1961, one of his first moves was to establish the Korea Electric Company by consolidating smaller, fragmented electric utilities under state control. KECO’s purpose was to provide stable, centralised power infrastructure that could support industrialisation and national development. Over the next two decades, it became the backbone of the country’s rapidly growing manufacturing economy, expanding the transmission network, building thermal power stations, and managing energy access in both urban and rural areas. KECO was the dominant utility provider, although smaller companies still existed. Like most countries at the time, electricity generation was fundamentally based on coal, but in 1972, KECO began construction of Kori 1, a 570 megawatt reactor designed and supplied by the American company Westinghouse. During the construction of Kori 1, KOPEC (Korea Power Engineering Company) was established in 1975 and became a wholly owned subsidiary of KECO. Its role was to build domestic capability in nuclear power plant design and engineering, especially for balance-of-plant systems. A second marginally bigger reactor, Kori 2, with a 640 MW capacity, began construction in 1977 with increased Korean participation in construction. After a slight delay, Kori 1 began commercial operation in 1978, eventually running until June 2017 and generating over 148.55 TWh during its lifetime. At the time, it cost around $300 million ($2.2 billion in 2025), resulting in a per MW cost of $3.8 million per MW in 2025 dollars. In 1982, KECO was reorganised and became the Korean Electric Power Corporation (KEPCO).

Kori 1, which supplied over 148.55 TWh of power from 1978-2017.

Unlike China, which began its civilian nuclear program using designs derived from military submarine reactors, South Korea’s program relied entirely on foreign expertise and civilian sector imports. Kori 1 was the only plant built on a full turnkey basis by Westinghouse, with limited domestic participation. As new reactors were commissioned, South Korean firms gradually expanded their roles in engineering, construction, and component supply. By the time construction began on Kori 3 in 1979 and Kori 4 in 1980, KOPEC had assumed responsibility for systems engineering, Hyundai and Daewoo were managing major civil works, and Doosan (then Korea Heavy Industries) was manufacturing reactor pressure vessels and steam generators under Westinghouse’s technical supervision. These projects, along with Yonggwang 1, which began construction in 1981, and Yonggwang 2 in 1982, both using Westinghouse’s three-loop PWR 950 MW design known in Korea as the WH F, marked the point at which KEPCO stepped into the role of overall project manager. These projects, which left Korea with a nuclear generation capacity of 5 GW in 1987 (but produced 49% of South Korea's 78.89 TWh of annual electricity demand), were all based on proven Westinghouse designs. By the late 1980s, Westinghouse had either directly designed or licensed over 50 three-loop PWRs (a type of pressurised water reactor which uses three separate coolant loops to transfer heat from the reactor core to steam generators, improving thermal efficiency and enabling larger reactor outputs compared to earlier two loop designs) in the US, Japan, South Korea, Spain, and Belgium. This successful global deployment influenced thinking in Korea that nuclear reactors had to be built in fleets of similar designs to smooth out design flaws, allow learning from all participants, and recoup the costs of the original designs.

In 1989, KEPCO began the construction of the first non-Westinghouse reactor, the System 80 1400 MW PWR designed by Combustion Engineering (who were later acquired by Westinghouse after they were bought by the Swiss/Swedish firm Asea Brown Boveri). The System 80 was both a step up in generation capacity and South Korean involvement. Although firms like Hyundai and Daewoo had already been managing civil works and KOPEC had taken on systems engineering, the System 80 reactors at Yonggwang 3 and 4 marked a deeper level of Korean technical participation. Doosan Group, a heavy engineering firm, under guidance from Combustion Engineering, manufactured reactor pressure vessels, steam generators, and pressurizers, mastering critical techniques in forging, welding, and non-destructive testing years ahead of China’s own efforts. While some components, such as reactor coolant pumps and control rod drive mechanisms, continued to be sourced from foreign suppliers, Korean firms rapidly took over installation, integration, and the production of auxiliary systems. KOPEC began managing plant-wide system integration and adapting digital platforms for Korean conditions, while KEPCO adjusted plant layouts, grid compatibility, and construction sequencing to suit domestic needs. Licensing and training documentation were localised, and small yet telling adaptations, like redesigned control room interfaces, showed growing institutional confidence. This broad-based localisation effort provided Korean industry with practical experience across the full range of nuclear-grade systems, forming the technical and institutional basis for the fully domestic OPR1000, and ultimately, the APR1400. These later designs not only retained core system continuity but also embedded lessons from the System 80 phase into standardised documentation, modular construction practices, and a streamlined regulatory process.

After the first wave of Westinghouse designs began construction and KEPCO concentrated on completing them, there was a six-year break in new reactor starts from 1983 until the Yonggwang/Hanbit 3 System 80 reactor was approved and began construction in 1989. A further pause from 1990 to 1993 as KEPCO coordinated the design of the OPR1000 units, while the South Korean economy continued to grow and required further power to fuel it, led to KEPCO expanding coal-fired generation, as well as opening new gas-fired plants. Although Korean nuclear plants were cheap and completed swiftly by international standards, as Korean energy demand grew by 8% annually from 1987, nuclear could not keep up the pace demanded. The Seoincheon Combined Cycle Power Plant, a 1800MW gas-fired power station that began construction in 1990, was completed in just two years for about one fifth of the cost of a nuclear plant. Although KEPCO was the central utilities provider, it operated through subsidiaries such as KHNP for nuclear energy and Korea Western Power (KOWEPO) for coal and gas generation, who lobbied for increasing expansion of their own generation.

The South Korean government began developing five-year Basic Rational Energy Utilization Plans starting in 1993 to address the growing energy demand and promote efficient energy use, and concluded that with South Korea's minimal natural resources, exposure to any single form of generation was too risky. In the context of the early 1990s as the shadow of Chernobyl lingered, although nuclear fuel could be stockpiled for more than five years, their future OPR1000 rollout might not be as successful as the previous generation of foreign designs and securing a diverse electricity supply that could match electricity demand growth was more important than lowering carbon emissions.

By the time the first OPR1000, South Korea’s domestically standardised reactor, entered operation in 1995 at Ulchin Unit 3, the country had already completed nine reactors using foreign designs from Westinghouse and Combustion Engineering. The OPR1000, also known as the Korean Standard Nuclear Power Plant, was Korea’s first fully sovereign design, an accomplishment only matched at the time by the US, Russia, France, Japan, and the UK. Being owned by KEPCO, it could have been sold without requiring foreign approval for export, but it never was, at an odd point in history when, despite increasing awareness of the downside of carbon-emitting electricity generation, there were not enough countries in a position to purchase it.

OPR 1000/Korean Standard Nuclear Power Plant

As part of continuous development, the eventual per-MW cost of the 12 units built settled around $2.5 million. However, revenue from selling nuclear-generated power and past successes meant that the development of the next-generation reactor, the APR1400, could begin in 1992. OPR1000 reactors continued to be built until 2008, when unit 2 at Shin-Wolsong started construction, and KEPCO began the rollout of the APR1400, which had been approved six years earlier. Continuing to construct OPR1000 units meant that costs were lowered for the overall fleet, component supply would continue for longer, and KEPCO had maximised the design costs.

The APR1400 was an evolution of the OPR1000, retaining the same core reactor technology as the OPR1000 but increased capacity to 1400 MW, added digital instrumentation and control, upgraded seismic resistance, and extended design life to 60 years. By maintaining consistency in the reactor core, documentation structure, and construction sequence, KEPCO and KHNP facilitated efficient regulatory review, shorter build times, and smoother supply chain coordination. Modular construction techniques, reduced field welding, and the ability to plan and build reactors in series helped Korea avoid the delays and cost inflation that plagued comparable Western projects, such as the AP1000 or EPR. The first APR1400 unit, Shin Kori 3, began construction in 2008. However, after the second unit started in 2009, there was a pause in nuclear reactor construction to assess whether the APR1000 would be as efficiently produced as previous designs.

High Margins, Low Friction, Global Reach

Although planning for new reactors continued at Shin Kori and Shin-Hanul, the 2011 Fukushima incident led to a pause in new reactors being brought online and a reduction in the plan to produce 65% of South Korea’s energy from nuclear power by 2035. The energy debate in legislative elections in 2012 and 2016, as well as in presidential elections in 2012 and 2017, centered on nuclear safety and the potential viability of variable renewable energy sources. Although President Moon Jae-in campaigned on a platform of phasing out nuclear in 2016, he decided to establish a citizens jury of 471 randomly selected South Koreans to vote on whether to restart construction of nuclear reactors at Shin Kori. Convened through the Prime Minister's office (Lee Nak-yon was selected for the office by Moon and had no particular links with the Korean nuclear industry) the citizens jury voted 59.5% voting in favor of restarting construction, while also endorsing a phase out of nuclear power over the longer term.

With the Fukushima incident significantly impacting nuclear construction in the 2010s, if KHNP had relied only on domestic construction, it might have suffered from staff attrition, loss of tacit knowledge, and a decline in institutional competence. However, as the APR1400 was a fully domestic design capable of export, it had won a contract for a nuclear power station in the UAE in 2009, beating rivals out on KHNP’s successful track record of completing projects on time and budget, and also promising to build up domestic Emirati skills and knowledge. Although the UAE has significant amounts of oil and gas, the then Crown Prince of Abu Dhabi, Sheikh Mohamed bin Zayed Al Nahyan, sought to diversify the economy and its electricity generation needs in addition to building up greater scientific, technical and civil engineering capacity. The Barakah nuclear power plant is now the UAE’s largest electricity generation source, costing approximately $18 billion for four APR1400 reactors, totaling 5.6 GW of capacity. Unit 4 started commercial generation in September 2024, so as of May 2025, annual figures for UAE electricity consumption show that in 2023, the 3-unit Bararkah plant supplied 24.5% of the Gulf nations' annual electricity. As the plants were completed on time and budget, and the UAE has signed deals with the United States to allow the UAE to import 500,000 of Nvidia’s most advanced AI chips annually and build data centers as large as those in the US, its continued power demand will likely lead to future reactors being built by KHNP in addition to the four existing plants and a further two announced in 2024.

KHNP’s Barakah project has been an undeniable success for both the company and the UAE. Although a prolonged pause in domestic reactor construction could have led to attrition in institutional capability, Barakah allowed KHNP to maintain its workforce, supply chain relationships, and engineering depth. Yet, as a subsidiary of KEPCO, KHNP’s international work was never financially existential to Korea’s nuclear industry. In fact, unlike every other national nuclear program, Korea’s nuclear sector is so cost-effective that KHNP routinely cross-subsidises more expensive fossil and renewable generation within the KEPCO system. Unlike China, which inflates the price of nuclear-generated electricity to help finance CNNC and CGN, the US where tax credits subsidise nuclear, and the UK which has set strike prices at rates up to $171.10 MWh (2025 prices, although contract-for-difference prices are nominally set in 2012 values, which in pounds is £92.50/MWh), Korean nuclear energy can make substantial profits for KHNP.

KHNP helps offset losses for KEPCO from coal, natural gas, and variable renewable generation by producing electricity from nuclear power cheaper than it is sold on the market. Electricity prices for consumers in Korea are set by the Ministry of Industry, Energy, and Trade. In 2025, the rate for industrial users was approximately 182.7 won per kilowatt-hour, or $0.13. Industrial electricity costs in Korea compare extremely favourably to Western European nations: in the UK, they were around $0.22 per kWh, and in Germany, $0.25 per kWh. These countries have opted for variable renewable-heavy grids with backup capacity supplied by gas, whose cost is exposed to global market volatility. In the United States, industrial power averaged $0.13 per kWh in 2024. In Asia, Korea compares favourably to Japan, where prices were $0.205 per kWh, although China maintains lower industrial tariffs at around $0.088 per kWh.

On a levelized cost of energy basis, which is suitable for technologies with stable and predictable generation over decades, KHNP’s nuclear fleet has an LCOE ranging from $44 to $63 per MWh. With Korean industrial electricity prices set at $130 per MWh, even the most expensive reactors in the fleet generate a gross margin of $67 per MWh, or 51.5%. At the low end, KHNP earns $86 per MWh, corresponding to a 66.2% margin. This extraordinary level of profitability is almost unheard of in global energy markets and helps explain why Korean nuclear generation is capable of cross-subsidising fossil and renewable generation within the KEPCO system, despite electricity prices being set by the state.

Korea’s success in low costs for nuclear generation is not because of the relatively uninterrupted cadence of construction. Although fleet designs spread the cost of component construction, South Korea’s approval, licensing, and planning processes minimize costs while maintaining stringent safety regulations. Compared to the arduous, multi-agency, and often sequential approval process that defines new nuclear development in Britain, South Korea’s system is significantly more streamlined, centralised, and policy-aligned. When KHNP seeks to build a new reactor, the approval process is comparatively streamlined and coordinated. It involves a small number of core regulatory steps managed by institutions with aligned policy objectives.

Reactor design approval is handled by the Korea Institute of Nuclear Safety (KINS), which assesses safety systems, containment, fuel integrity, and radiation control. For standardised reactors such as the APR1400, which have already received domestic certification, this step can be completed swiftly. In parallel, the Ministry of Trade, Industry and Energy (MOTIE) manages the construction permit and development approval, ensuring that licensing is integrated with national electricity policy and energy planning.

Environmental scrutiny is delivered through a single Environmental Impact Assessment (EIA), overseen by the Ministry of Environment. Unlike in the UK, where environmental review is split across multiple agencies and stretched across a sequence of stages, Korea’s EIA is specific to the project and typically proceeds in parallel with other approvals. It examines ecological effects, seismic risk, water use, and radiological protection, and is coordinated with both MOTIE and KINS to prevent regulatory duplication and delays.

The UK process is markedly more fragmented and protracted. Developers must undergo three separate tracks: a Generic Design Assessment (GDA) by the Office for Nuclear Regulation (ONR) and the Environment Agency (EA), a Development Consent Order (DCO) process led by the Planning Inspectorate, and a series of environmental permits issued by the EA for emissions, waste, and water use. Each stage has its own public consultation requirements and is rarely coordinated with the others. The GDA alone can take four to five years and is not site-specific, requiring repetition when a project proceeds to location-specific planning. Sizewell C, a two-reactor 3.2 GW plant under construction in the UK, required more than 43,000 pages of environmental documentation to be submitted in only one of these processes. Importantly, the ONR does not have a statutory mandate to deliver new nuclear capacity and is focused solely on safety regulation. Oddly, it does not sit within the British Energy department (DESNZ) but is the responsibility of the Work and Pensions Ministry. By contrast, Korea’s Nuclear Safety and Security Commission (NSSC) plays an explicit policy-aligned role in nuclear expansion as part of national strategy.

The result is a stark difference in delivery timelines. Hinkley Point C will take roughly 22 years from initial regulatory engagement to first power. In South Korea, KHNP can license, construct, and commission an APR1400 reactor in less than half that time, owing to standardisation, political coordination, and institutional alignment.

The installation of Shin Kori 5's reactor vessel in 2019.

The future of KEPCO.

In 2025, South Korea’s nuclear capacity stands at approximately 25.6 GW, with plans to increase this to 28.9 GW by 2030 and 31.7 GW by 2036. The election of President Yoon Suk-yeol in 2022 marked a significant policy shift, abandoning former President Moon Jae-in’s ambition to phase out nuclear power. However, Korea’s longer-term plans still limit the expansion of nuclear power to 35% of electricity generation by 2038, despite its low cost, reliability, and potential to hedge against supply disruptions as Korea still regards it too risky to totally rely on a single generation source and the legacy of the 2013 policy shift to reduce nuclear generations. To limit carbon emissions, Korea currently plans to phase out coal and gas by 2050 (it still expects to generate 10% from coal and 10% from gas in 2038), expand variable renewable generation to 77.2 GW of solar and 40.7 GW of wind by 2038, and, similar to Japan, anticipates the emergence of commercially viable hydrogen generation technologies, despite its dubious prospects.

In addition to 117.9 GW of variable renewable (VRE) generation ($54.6 billion in new investment for solar, $202.2 billion for wind based on on South Korean LCOE estimates of $113 per MWh for solar and $189 per MWh for wind), the South Korean government has also proposed installing 138 GWh of battery energy storage systems (BESS) costing an estimated $22.8 billion. In addition to grid infrastructure expansion, upgrades, smart grid investments, and solar and wind installation costs, this would require $23.83 billion annually until 2038. While some of these costs may decrease, particularly battery costs, which are manufactured by South Korean firms LG Energy Solution, Samsung SDI, and SK On, the likelihood of wind turbine costs falling substantially after mainly European countries have piled hundreds of billions in subsidies for wind turbine development is limited. While KEPCO still dominates the electricity market in South Korea, the vast majority of South Korea's 29 GW of solar generation is not provided by KEPCO but by independent power producers (IPPs) who are subsidised with fixed prices and state targets for renewable-sourced electricity, which guarantees them market share, but the envisaged wind expansion is due to fall on KEPCO’s subsidiaries (Korea South-East Power, Korea Midland Power, and Korea Western Power).

The South Korean government does plan to directly subsidise some of this transition and has planned $6.8 billion of central government investment annual by 2030, but the vast majority of the cost will fall on KEPCO, which suffered a $24.6 billion loss in 2022, a $3.43 billion loss in 2023 and has debts over $141.5 billion. Although the losses in 2022 and 2023 were due to of high fossil fuel generation costs, the plans to not phase them out until after 2038, continuing to expose them to future losses, the massive amounts of VRE capital investment and global experiences of VRE instability (VRE only contributes 6% of annual electricity production at the moment) Korea may yet return to its aims of 65% of electricity coming from nuclear energy.

To reach 65% of a projected 2038 electricity demand of 129.3 GW, this would require building a total of approximately 84 GW of new nuclear capacity. This would require three APR 1400 reactors to come online every year by 2038, with a capital cost of roughly $181 billion to $198 billion over the build period, which is cheaper than the proposed 40.7 GW of wind capacity and avoids most of the grid infrastructure costs.

As nuclear reactors are far smaller than VRE generation sites and can be located close to existing industrial and population centres rather than where the weather is most suitable, although this would be a massive expansion of nuclear construction, KNHP and its component suppliers could achieve this. As South Korea backs new nuclear generation with state-backed loans and nuclear generates profits for KNHP and KEPCO overall, it would be far more fiscally sustainable than the proposed VRE expansion and less risky than relying on natural gas costs. Although coal-fired stations in Korea are supercritical, meaning they operate at higher temperatures and emit fewer particulates (PM2.5 and PM10, nitrogen oxides, sulfur dioxide, and mercury), compared to nuclear power, coal stations have far lower capacity rates (averaging around 60%) and produce significant amounts of carbon emissions. Moving to a far higher nuclear generation goal would require not only a reassessment of the risk of relying to heavily on a single generation source, and long term political backing which is tricky to achive amidst domestic political unheaveal, but KNHP could deliver it, the expansion would be likely cheaper than the alternative and it would reduce Korean carbon emissions in an achievable manner while not affecting domestic electricity prices of South Koreas manufacturing heavy economy.

Away from potential grid-scale expansion, KEPCO E&C (Engineering & Construction) and KAERI (Korea Atomic Energy Research Institute) are working on small modular reactors intended primarily for industrial applications such as process heat, desalination, and electricity in remote areas or small grids. Their flagship SMR is the System-integrated Modular Advanced Reactor (SMART), which can generate 110MW of power, smaller than Rolls-Royce’s proposed 470 MW reactor or CNNC’s Linglong One (ACP100), a 125 megawatt design due to come online in 2026. Although KHNP signed an agreement with Saudi Arabia’s King Abdullah City for Atomic and Renewable Energy (K.A.CARE) in 2015 to provide SMART, the project has stalled. (CHECK). KHNP, Doosan Enerbility, and Kepco E&C are also working on the 170MW i-SMR for further export potential in Indonesia and Jordan. However, High-Temperature Gas Reactors and Sodium-cooled fast reactors being developed in China are not currently research priorities for Korea. Just as the APR1400 was an evolution of previous designs, since 2009, KHNP has been developing a successor design with a slightly larger capacity, 1500 MW, and an even longer design life of 80 years. However, it is unlikely to begin deployment until KHNP has recovered all the costs of developing the APR1400.

Implications and weaknesses.

South Korea’s primary weakness in its nuclear industry supply chain is the lack of domestic uranium production or any refining or enrichment facility. KEPCO Nuclear Fuels is the subdivision responsible for procuring fuel for nuclear reactors. All natural uranium is imported, typically as uranium oxide concentrate (U₃O₈). In 2022, Korea imported approximately 4,600 tonnes of uranium, primarily from Kazakhstan, Canada, and Australia. Korea lacks any indigenous uranium enrichment capability due to its commitments under the U.S.–South Korea 123 Agreement, renewed in 2015. All enrichment services are contracted externally, typically with companies in the United States, Europe (Urenco), and Russia. The fuel cycle process, therefore, requires Korea to import uranium, export it abroad for conversion and enrichment, and then reimport the enriched uranium. KEPCO Nuclear Fuel operates a fuel fabrication plant in Daejeon with an annual capacity of around 650 tonnes of fuel assemblies, where the reimported enriched uranium is processed into reactor-ready fuel. This structure leaves South Korea strategically dependent on external partners for upstream stages of the fuel cycle, even as it maintains strong domestic capabilities in fuel fabrication and reactor operation.

Although South Korea has a deep military industrial base, including the capacity to build missiles, satellites necessary for target identification and guidance, sophisticated research reactors, advanced radiochemical laboratories, and a skilled nuclear workforce, its lack of enrichment facilities for civilian or military-grade fuel means it is not in the same position as Japan to rapidly acquire nuclear weapons, a process which some analysts estimate Japan could complete in as little as six months. South Korea does possess approximately 0.7 tonnes of separated plutonium stored abroad, primarily in the United Kingdom and France, as a result of overseas reprocessing agreements. In theory, this amount could yield around 100 to 130 nuclear warheads with yields in the range of 10 to 20 kilotons, depending on the design. In reality, getting the plutonium stored abroad, which is closely monitored by the authorities there and also the IAEA, back to South Korea to place it in warheads is not feasible. While the South Korean population is overall favourable to acquiring nuclear weapons, and South Korea has repeatedly asked the US to again position nuclear weapons in the country (which it did prior to 1991) in response to North Korea's nuclear program and the growing military sophistication of China's military and growing nuclear forces, the government has remained formally committed to non-proliferation. The real strategic value of South Korea’s civilian nuclear program lies not in latent weapons capacity, but in its economic benefits and energy resilience it provides.

Conclusion

South Korea’s nuclear industry stands as a rare example of sustained, coherent industrial policy. Decades of steady investment, consistent reactor design, and political alignment have produced a fleet that delivers low-cost, low-carbon, and dependable electricity. Crucially, Korea has maintained institutional expertise and supply chain depth, avoiding the stagnation and disruption seen in many Western countries where fragmented regulation, rising costs, and inconsistent political support have undermined nuclear energy. Rather than being a financial burden, Korea’s reactors play a stabilising role in the power system, insulating industrial users from global gas price shocks and offsetting losses elsewhere in the electricity market.

But the outlook is uncertain. Official targets to cap nuclear’s share at 35 percent by 2038 are hard to square with its economic and environmental strengths. As KEPCO takes on more high-cost variable generation, the risk is that it drifts into the same cost pressures and system reliability issues that have plagued other energy systems dominated by renewables. Korea has the technical capacity and industrial base to expand its nuclear fleet if it chooses. Failing to do so would echo the mistakes made elsewhere, where political hesitation has hollowed out once-strong nuclear programs and made decarbonisation harder and more expensive.

Good article! I recommend using square brackets for things you want to go back to though (to make control f easier!):

Although KHNP signed an agreement with Saudi Arabia’s King Abdullah City for Atomic and Renewable Energy (K.A.CARE) in 2015 to provide SMART, the project has stalled. (CHECK).